The long-term debt cycle

Recently I’ve been learning more about the rhythm of long-term debt cycles. This writing is my attempt to better understand the topic.

———

Most people are familiar with normal 5-10 year “boom and bust” business cycles. These are characterized by multiple years of economic growth followed by a catalyzing event which triggers a period of deleveraging known as recessions. The catalyzing event could be internally induced, which is what happened during the great financial crisis. They can also be externally induced like earlier this year with the coronavirus. For Americans, these multi-year oscillations in the economy are imprinted in the fabric of our daily lives. They are familiar and normalized.

But what is more interesting to me these days is what will happen at end of a long-term debt cycle. Unlike standard business cycles, a long-term debt cycle is much more amorphous because most of the living population in the developed world (G7 democracies) have never directly experienced it.

A lot of macro economists and traders have been sounding the alarm that our global economy is at the precipice of a significant long-term debt cycle unwinding. So it felt important that I pay attention.

So what exactly is it?

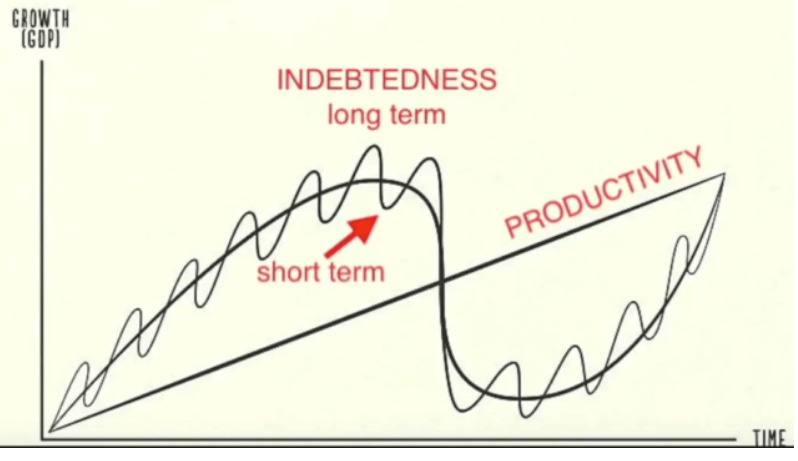

The concept of a long-term debt cycle was popularized by Ray Dalio to describe an economic phenomena that occurs every 50-100 years. The big idea is that after each recessionary period in the economy, the debt levels as a percentage of GDP increase from its previous base line.

After each successive standard business cycle, so much debt builds up in the system that the economy will inevitably hit a breaking point.

The main way to tell the end of a long-term debt cycle is looming is when federal interest rates hit the zero bound. Low to no interest rates are a precursor to central banks and governments reverting to non-traditional measures in order to stimulate economic activity. We saw a lot of this in 2020.

Why do long-term debt cycles happen?

The real answer to this question fascinated me because it ultimately boils down to human behavior. Many people assume long-term debt cycles happen because of broken governments and economic systems. And while those are factors which play into how acute the debt problem becomes, they are not the main reason.

In reality, super cycles of debt accumulation and deleveraging have occurred for thousands of years in human history.

A curious theme among societies that use monetary energy to drive economic vitality is an indomitable will to grow at all costs. In other word, greed.

When the economy is pushed too far and a collapse is triggered, the natural response for governments is to fix the problem as quickly as possible. There is a lot of merit to this reaction. Recessions cause a lot of pain and suffering. Short-term measures might be an answer within the context of a standard business cycle, but the underlying debt it creates in the system does not go away. It’s merely kicking the can down the road.

Long-term debt cycles and wealth inequality are tightly correlated

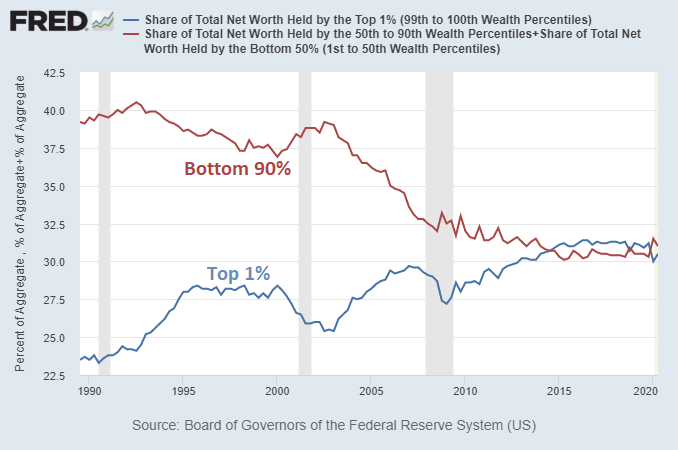

If long-term debt cycles have been happening for thousands of years, it was not surprising when I learned these cycles are tightly correlated with wealth inequality. A widening wealth gap between the working class and ruling class is also a phenomena that goes back thousands of years. It makes sense given capital has a tendency to compound exponentially while labor accrues linearly. People with capital can build wealth at a different rate than those without it.

In the United States, there are conditions which have exacerbated this problem over the last 50 years. For example, in 1971 when President Nixon ended Bretton Woods and moved off the gold standard (and eventually re-pegged to the petrodollar), it resulted in a sharp divergence in productivity and wage compensation.

When the US shifted to the petrodollar it quickly made the country into a net-exporter nation, meaning it off-shored a lot of it’s manufacturing and labor. This created ideal conditions for wealth inequality to run rampant on shore. Business owners learned how to boost productivity while becoming more cost-effective thanks to offshore labor arbitrage and new technology. The working class onshore did not benefit from these productivity gains.

If we look back over the past 3 decades from 1990 to present, the widening wealth gap is stark and eye-opening:

As we move beyond the the first year kicking off the 2020’s, it will be interesting to see how far the wealth gap will continue to grow in American and how the long-term debt deleveraging period— whenever it really starts kicking in— will accelerate shifts in wealth redistribution and radical policy changes. The social, cultural and political discourse has already been heating up intensely this year.

The different types of monetary policy

During periods of high economic uncertainty, central banks have several measures of monetary policy at its disposal to prevent catastrophe. These policies are generally broken down into 3 types, often referred to as MP1, MP2 and MP3. It’s worth understanding these different forms of policy to frame what is happening today.

Monetary policy 1 (MP1) — Involves controlling interest rates to stimulate or curb inflation. As a long-term debt cycle plays out, the interest rates go lower and lower each cycle trending towards zero.

Monetary policy 2 (MP2) — This comes into effect when interest rates have hit zero. Central banks must print money as bank reserves and use the money to buy assets like gov't debt and corporate bonds.

Monetary policy 3 (MP3) — Comes into effect after zero interest rates and gov't has started buying a lot of assets. The central bank begins coupling with the government on fiscal spending. M3 is more targeted to consumer spenders versus investors.

MP1, MP2 and MP3 are typically activated in successive order. MP2 occurred a lot this year as the FED bought a lot of treasury and corporate bonds directly. We also saw a fair amount of MP3 this year when the FED partnered closely with congress (bridging monetary policy + fiscal spending) to print $2T and deploy it to people through the CARES act and PPP. And just this week we saw an addition $800B stimulus bill pass for broad continued support.

The problem is not that the printing won’t stop. The problem is that it can’t stop.

The last deleveraging from a long-term debt cycle in America was all the way back in the 1930s and 1940s during WW2. But it's very difficult to compare today and that era because the world is a completely different place.

A major problem for the US in trying to stimulate growth and moderately targeted inflation (of ~2% per year) in today’s environment is that our society is overwhelmingly engulfed by two powerful deflationary forces: trade (and to be specific, labor arbitrage) and innovation driven by tech.

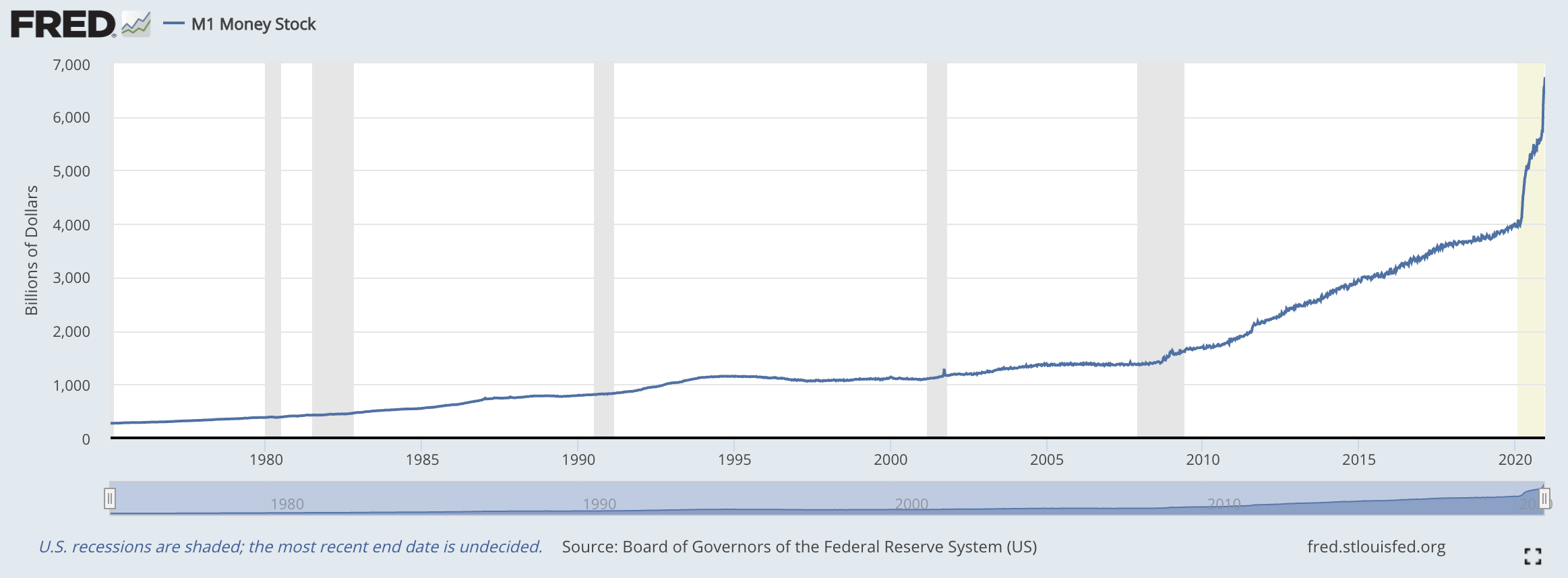

This essentially means the government will need to continue printing exponentially more money in order to counter the deflationary forces growing exponentially stronger to try and reach the baseline equilibrium. Federal balance sheets ballooning from billions to trillions is already concerning enough. This debt is assuredly only going to keep going up as made evident by this chart of the long-term M1 money supply:

If technology is a deflationary force that will continue to disrupt and disintermediate every single industry at, in my view, an exponentially faster rate, then governments really have no choice. They have to keep money printing to prop up the system from collapsing. This was a dilemma even before the coronavirus. Now the problem is even more magnified.

Final thoughts…

One of the reasons I've been learning more about the long-term debt cycle is because I am trying to understand what things will look like over the next decade.

The answer to when mass deleveraging from the current long-term debt cycle will happen is largely predicated on fiscal policy. And contrary to the natural belief that it’ll happen overnight, I think it will play out slowly over years. This is how it unfolded in the 1940s — as a gradual unwinding.

It will be interesting to see how modern economies will come out the other side. Time will tell. I tend to lean towards optimism and hope the US is headed towards a more equitable world. But the rational side of me knows there will be a lot of dark days and pain on the road to getting there.

One thing is certain. The 2020s will be an intensely uncomfortable ride.